Welcome to the Weekly SUMmary - 12/04/2020

As we put a close on one of the wildest years we've ever seen, those that have the ability to do so should consider contributing to a retirement plan. Below are just a few reasons to do so.

- Tax benefits!

- If you contribute to a pre-tax account, you reduce your income for the year dollar for dollar. Say you were a married couple on pace to make $100,000 for the year. You each decide to contribute $5,000 to your IRA, poof! your income now looks like $90,000 for tax purposes, BUT every penny you put into that account is your money that has the potential to grow* with time.

- If you contribute to a Roth, unless it's in a work retirement account you've likely already paid taxes (through work payroll) on those funds, so you can deposit into your Roth and watch its tax deferred growth potential with eventual tax free distributions1. For more info on Roths, see here.

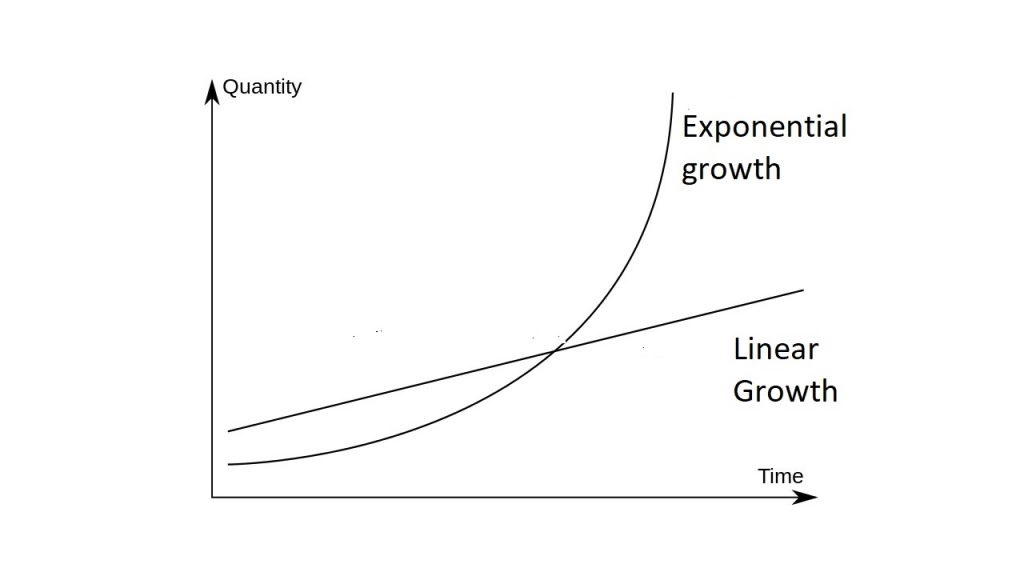

- Compound growth!

- Simply put, with time, your money should grow*. The money that grows can then grow more money. That money can grow, and so on. This is why you see exponential growth charts, because of the compounding effect.

- If you did not invest your money, but had it in a sock drawer and continued to put the same amount of money in it each time, without potential growth, the overall amount you have would rise similar to the Linear Growth line here. When you invest and as long as it grows, eventually, with compounding, your line should look more similarly to the Exponential Growth line.* Another argument against the Linear option would be inflation, but that's a topic for another conversation.

- To keep you from spending it!

- This is obviously the most painful part of the conversation. If I've learned one thing during my time in this industry, it's that people will find something to spend their money on unless they do not have immediate access to it. Although it may be painful in the near term, making the decision to contribute is in almost2 everyone's best interest in the long term. As mentioned earlier in this blog, the funds/assets are still yours. They have growth potential. You will be able to take distributions and use those funds in the future.

*Investing involves risk, including the potential for loss of principal. Generally, the greater an investment's possible reward over time, the greater its level of price volatility or risk.

The hypothetical chart is for illustration purposes only and is not intended to be representative of actual results or any specific investment, which will fluctuate in value. The determinations made by this example are not guarantees or projections, and no taxes or fees/expenses are included in the calculations which would reduce the figures shown.

If you withdraw money from a traditional IRA before age 59½, your deductible contributions and earnings will be taxed as ordinary income. You may also be subject to a 10% penalty on early withdrawals. Please discuss with your tax advisor prior to making financial decisions.

Roth IRA contributions are subject to income limitations.

1. Tax free distributions are based on qualified distributions. More explanation can be found here, or via the IRS website.

2. "Almost" refers to those that may be in debt to the point where paying that would be much more beneficial than making a contribution. For example, if one has debt on a credit card, paying 20% interest, the possibility to grow at a rate faster than 20% is highly unlikely (historically speaking), therefore, it is likely more beneficial to pay off the debt before investing.

As usual, these posts are meant to be educational in nature and the content provided is based on advanced education and experience in the financial services industry. This should not be considered investment advice, nor does it constitute a recommendation to take a particular course of action. Please consult with a financial professional regarding your personal situation prior to making any financial related decisions.

(12/20)